For the better part of a decade, the narrative in accelerated computing has been singular: NVIDIA is the market. To build AI, you bought green. But the tectonic plates of the industry are shifting. The recent announcements from Hewlett Packard Enterprise (HPE) and AMD at HPE Discover are not just product updates; they are the blueprint for a new, multipolar AI world order.

By committing to AMD’s “Helios” architecture and securing the massive “Herder” supercomputer contract, HPE is signaling that the era of the single-vendor monopoly is drawing to a close. This is the news the enterprise has been waiting for.

The Rise of the Alternative: AMD’s Moment

AMD has successfully transitioned from being a “second source” to a “go-to alternative.” The announcement that HPE will adopt the AMD “Helios” architecture—an open, rack-scale AI platform—for release in 2026 is a massive vote of confidence. This isn’t just about slotting in a different GPU; it’s about building an entire ecosystem around AMD’s roadmap, including the Instinct MI430X GPUs and next-gen EPYC CPUs.

We are seeing this momentum ripple through the market. Just days prior, cloud provider Vultr announced a massive expansion, launching an AI supercluster with 24,000 AMD Instinct MI355X GPUs. Vultr’s commitment to an all-AMD full stack—from EPYC CPUs to Instinct GPUs—demonstrates that for cloud providers watching their margins and power budgets, AMD is no longer a risk; it is a competitive necessity. AMD has provided the hardware performance to rival NVIDIA’s H100 and Blackwell, but more importantly, they have demonstrated the supply chain stability that enterprises crave.

HPE’s Strategic Pivot: Owning the Enterprise AI Stack

HPE has been quietly orchestrating a pivot that is now paying dividends. Moving beyond simple hardware box-shifting, HPE is positioning itself as the premier provider of hybrid and on-premise AI. Through its GreenLake platform, HPE offers “AI as a Service” that resides in a customer’s own data center—crucial for industries like healthcare, finance, and government where data sovereignty is paramount.

This new partnership accelerates that effort. The “Herder” supercomputer for Germany’s High-Performance Computing Center Stuttgart (HLRS), built on the HPE Cray GX5000 platform, represents the pinnacle of this strategy. Scheduled for the second half of 2027, Herder will deliver sovereign AI capabilities using AMD’s open ecosystem.

{kind=link}

For HPE, this is about differentiation. In an NVIDIA-centric world, OEMs often struggle to add value because NVIDIA dictates the entire stack—from the GPU to the networking (InfiniBand). By partnering with AMD, HPE can integrate its own IP. The “Helios” racks will feature HPE Juniper Networking switches developed with Broadcom. This allows HPE to sell a solution that is uniquely HPE’s, rather than just repackaging a standard NVIDIA DGX pod.

The Chinks in the Armor: Why NVIDIA Is Exposed

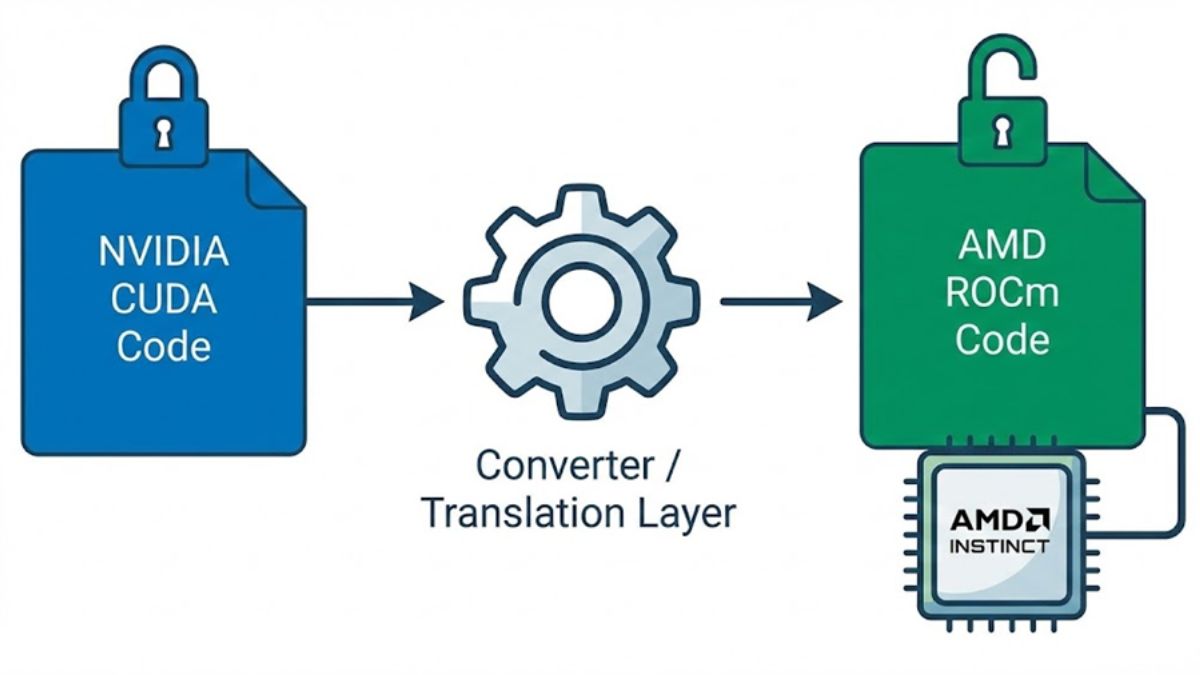

NVIDIA’s dominance has been built on two pillars: hardware supremacy and the software moat of CUDA. Both are under siege. The hardware gap has closed, but the erosion of the software moat is the more existential threat.

For years, “it runs on CUDA” was the gatekeeper. But companies like Spectral Compute (with its SCALE compiler), AMD (with HIPIFY and ROCm improvements), and tech giants like Microsoft are dismantling this barrier. They are building converters and abstraction layers that allow code written for CUDA to run seamlessly on ROCm. Microsoft, arguably NVIDIA’s largest customer, has been vocal about this shift. Its heavy investment in frameworks like Triton and ONNX is designed to commoditize the underlying hardware, making the GPU interchangeable.

{kind=link}

Furthermore, NVIDIA’s historic lack of focus on the enterprise—prioritizing hyperscalers like Meta and Google—has left traditional corporate customers feeling neglected. High prices, allocation struggles, and a rigid “take it or leave it” ecosystem have fueled dissatisfaction. Microsoft’s CTO, Kevin Scott, has famously hinted at the necessity of alternatives to keep costs in check. When the world’s largest software company is actively funding your competitors to break your lock-in, your exposure is real.

The Power of Partnership: Responsiveness as a Weapon

This is where AMD’s “unique advantage” comes into play: responsiveness. NVIDIA operates like a walled garden; AMD operates like a public park.

AMD’s willingness to embrace open standards (like the OCP Open Rack architecture used in Helios) and collaborate deeply with partners gives it a strategic edge. AMD allows partners like HPE to be partners, not just distributors. By letting HPE integrate Juniper networking and Broadcom silicon into the Helios stack, AMD is enabling HPE to maintain its own margins and technical identity.

This flexibility allows HPE to solve specific customer problems—such as power efficiency, liquid cooling, and specific networking protocols—in ways that a rigid NVIDIA reference architecture might not allow. In the enterprise market, where customization and integration are key, this responsiveness is a killer app.

Wrapping Up

The HPE and AMD announcements mark a turning point. We are moving away from a hardware monarchy toward a diverse federation of choices. HPE is leveraging AMD’s open ecosystem to fuel its hybrid cloud ambitions, while AMD is using HPE’s enterprise reach to cement its status as the true alternative to NVIDIA. For the CIO and the data center architect, the message is clear: The monopoly is over. You finally have a choice.

- The Breaking of the Monolith: How HPE and AMD Are Rewriting the AI Script - December 11, 2025

- Intel’s Hiring of Wei-Jen Lo: A Strategic Homecoming, not a Trade Secret Heist - December 2, 2025

- The Unlikely Savior of the AI PC Ecosystem: Why the Lenovo IdeaCentre Mini x (Snapdragon) Matters - November 26, 2025